Quebecers’ mortgage payments will rise due to a fifth consecutive increase in the key rate. And they are not at the end of their sentences, because it is not the last.

• Also Read: The Bank of Canada raised its key rate to 3.25%

• Also Read: Rising interest rates: All the more reason to avoid “orange taxes,” says Legault

• Also Read: Key rate hike: “You’ve got to get used to tightening your belt”, fears trustee in bankruptcy

The Bank of Canada (BoC) yesterday underlined that the jump from 0.25% to 3.25% in a few months will make mortgages cost more than car loans, credit cards and lines of credit.

But how much, exactly? News magazine A lot of experts were asked to do the math yesterday.

“It’s coming more realistically into borrowers’ pockets,” said Philippe Simard, director of mortgages in Quebec at Ratehub.ca, which landed in Quebec in 2015 and handles $600 million. Here are mortgage loans.

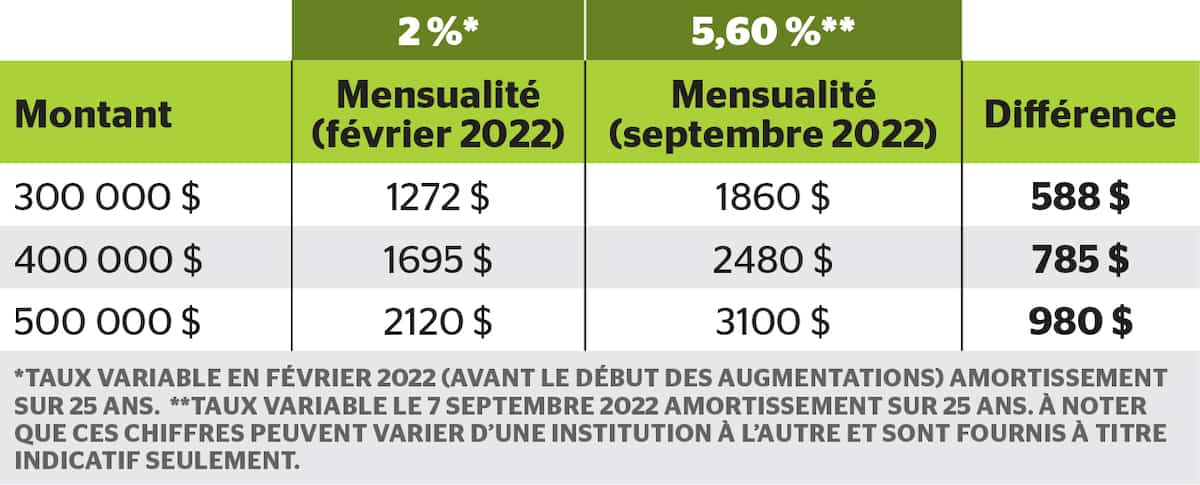

A longtime broker gives the example of a $350,000 mortgage with a 1% variable rate down. Last January and February, the amount due each month was $1390.

With five consecutive hikes by the BoC, the lowest rate Ratehub currently offers is 4.25%. For the same mortgage and with the same down payment, we’re now talking about a $1,927 payment, an increase of $537 or 39%.

“That’s definitely the Bank of Canada’s intention. They want people to stop using. If there’s a hole like this in the budget, there’s definitely going to be an impact,” he said.

When we consult another expert, trustee Pierre Fortin, president of Jean Fortin & Associates, we find more or less increase in payment.

A bit scary

For a $500,000 mortgage, even the numbers are scary. We went from a monthly payment of $2,120 at the beginning of the year to $3,100 today, a difference of $980 per month.

Photo taken from LinkedIn

Pierre-Antoine Harvey, Associate Researcher at IRIS

Before the pandemic, it was rare to see a $500,000 mortgage. But since then, this amount is not unusual.

In the past 24 months, more than half of first-time buyers have opted for a variable rate, CMHC said.

If they are significantly lower than the fixed rate, this is no longer the case.

“It’s clear that many employers will have to tighten their belts to receive the nearly $1,000-a-month increase since last March,” Lets Business Manager said.

When will it stop?

And it’s not over, as the BoC said yesterday that the key rate “may need to be raised further”.

Inflation is still at a 40-year high. This was 7.6% in July, a slight decline from 8.1% in June.

“There is still plenty of time to return to stable inflation at 2%, which is the BoC’s target,” Hendricks Vachon, senior economist at Desjardins Group, said yesterday.

For him, the 75 basis points increase announced yesterday was “huge”, as “normally we see a 25 basis point increase”.

In the context of inflation, however, “it’s a very strong pace, but it’s still justified.”

Patience, says Iris

Another story with Pierre-Antoine Harvey, economist and associate researcher at IRIS.

“One of the solutions is patience. Most of the inflation is due to the cost of energy, which is slowly coming down,” he explained.

Because if the BoC wants to curb inflation, it will do so at the expense of the poor, which reminds me of IRIS for some time.

“What’s troubling is that no one at the central bank has asked the question of whether historically high corporate profits play a role,” the economist continues.

He knows one thing for sure: like oil companies, banks are quick to raise prices, but slow to lower them when the time comes.

Examples of mortgage loans

More Stories

Cuba Launches Power Restoration After Third Nationwide Grid Collapse in a Month

Sportswear: Lolle acquires Louis Garneau Sports

REM is still innovative enough to foot the bill