In 2023, an individual will not pay taxes if their net taxable income is less than 16,372 euros in the year. For a childless couple, i.e. 2 shares per tax family, the net taxable income must be less than 30,558 euros to avoid being taxed.

As always, it is the number of shares in the tax family that affects the tax-free threshold. For example, a person living alone with children (1.5 tax shares) does not pay taxes if he declares a net taxable income of less than 21,760 euros for the whole of 2022.

Below €16,372 in 2022, a person pays nothing

To calculate the threshold of non-taxation, it is necessary to take into account the total income (salaries, pensions, rent, etc.) of the previous year, but also property and professional deficits and any allowances and deductible expenses.

The higher the number of shares in the tax family, the higher the tax-free income threshold. In the case of a single person and a household with 5 tax shares, the non-taxation threshold is 59,480 euros.

| Number of parts | A single person | A couple is subject to joint taxation |

| 1 | €16,372 | — |

| 1.5 | €21,760 | — |

| 2 | €27,149 | €30,558 |

| 2.5 | €32,537 | €35,947 |

| 3 | €37,926 | €41,335 |

| 3.5 | €43,314 | €46,724 |

| 4 | €48,703 | €52,112 |

| 4.5 | €54,091 | €57,501 |

| 5 | €59,480 | €62,889 |

How to calculate your tax rate for 2023?

If your net income for the year 2022 exceeds one of the above thresholds (depending on your family size), you will have to pay income tax. Below, we have put the details of tax scale according to family multiplier. These amounts take into account a 10% deduction on declared salary (or deduction of actual expenses).

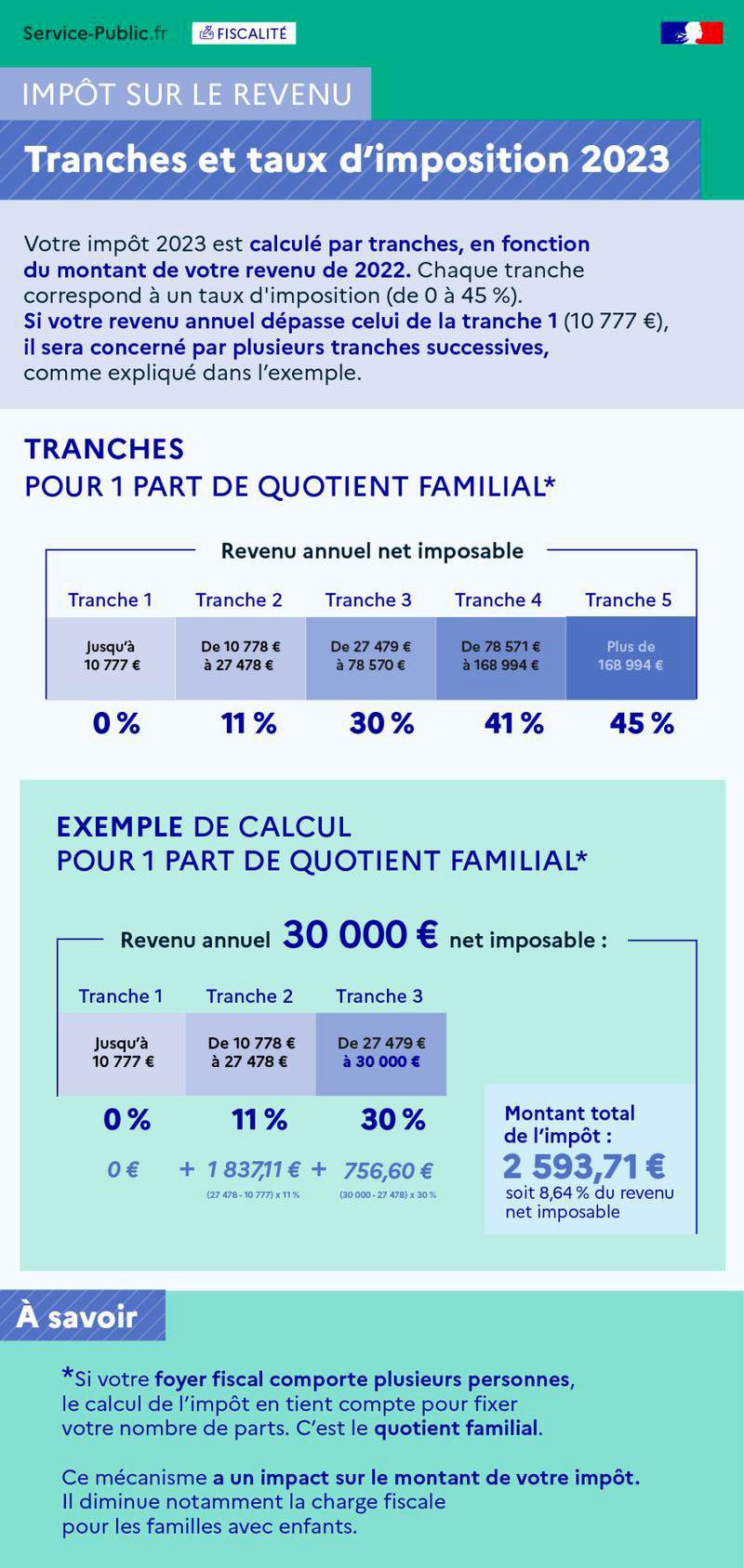

- For a household below €10,777: no tax

- For family quota between €10,778 and €27,478: 11% tax

- For family quota between €27,479 and €78,570: 30% tax

- For family quota between €78,571 and €168,994: 41% tax

- For family quota above €168,994: 45% tax

To give you an example, here is a calculation that applies to a single person (single, divorced, separated or widowed) earning 50,000 euros per year with a 10% discount. It is taxed at 0% for the portion between €0 and €10,777, then 11% between €10,778 and €27,478 and finally 30% between €27,479 and €50,000. The tax rate is not withdrawn on amounts below each level.

© Public Service

More Stories

Cuba Launches Power Restoration After Third Nationwide Grid Collapse in a Month

Sportswear: Lolle acquires Louis Garneau Sports

REM is still innovative enough to foot the bill